Study 7: A European Version of the PPCI

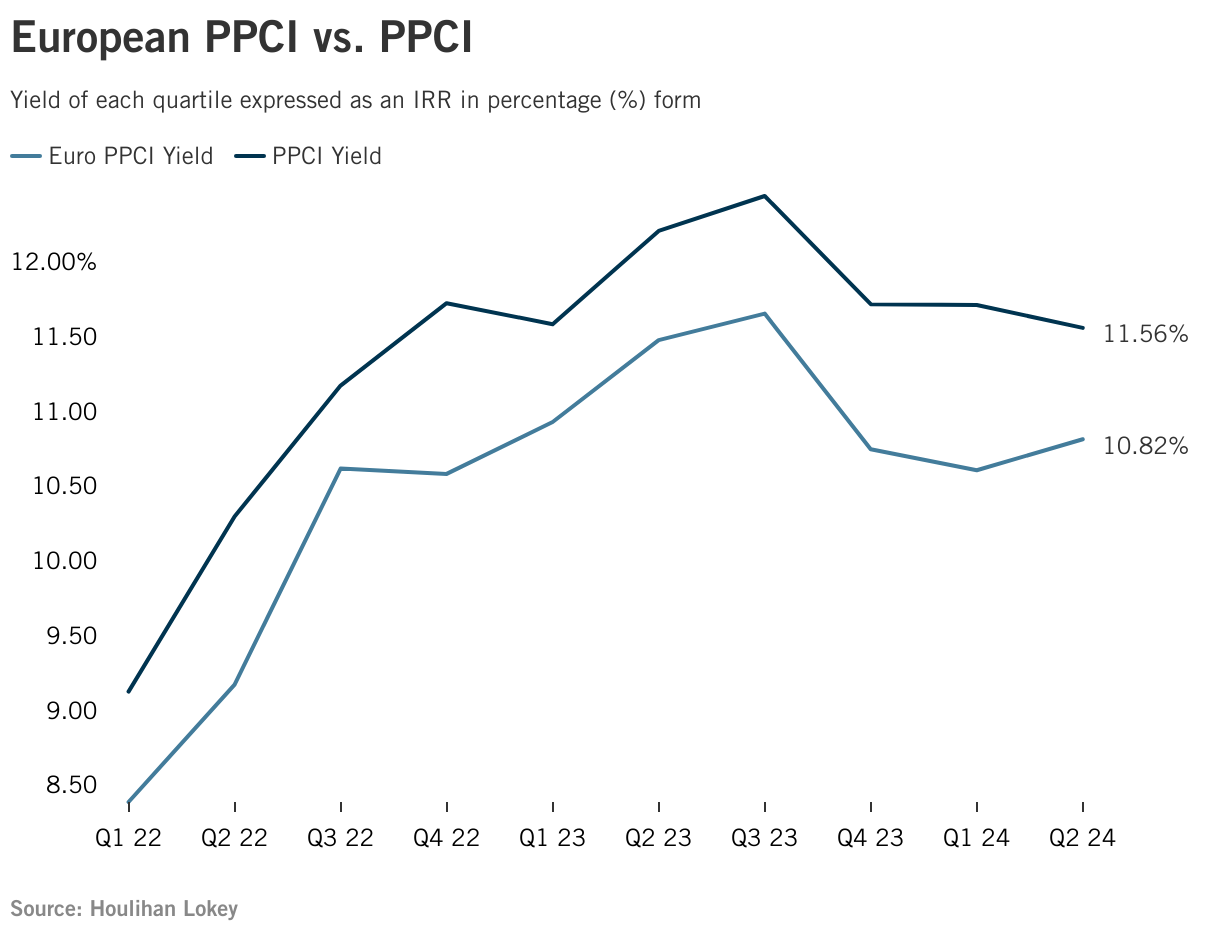

The Private Performing Credit Index contains loans with base rates other than SOFR. We have isolated the European base rate borrowings and calculated the weighted average yield with the same methodology as the PPCI.

Spreads and Prices

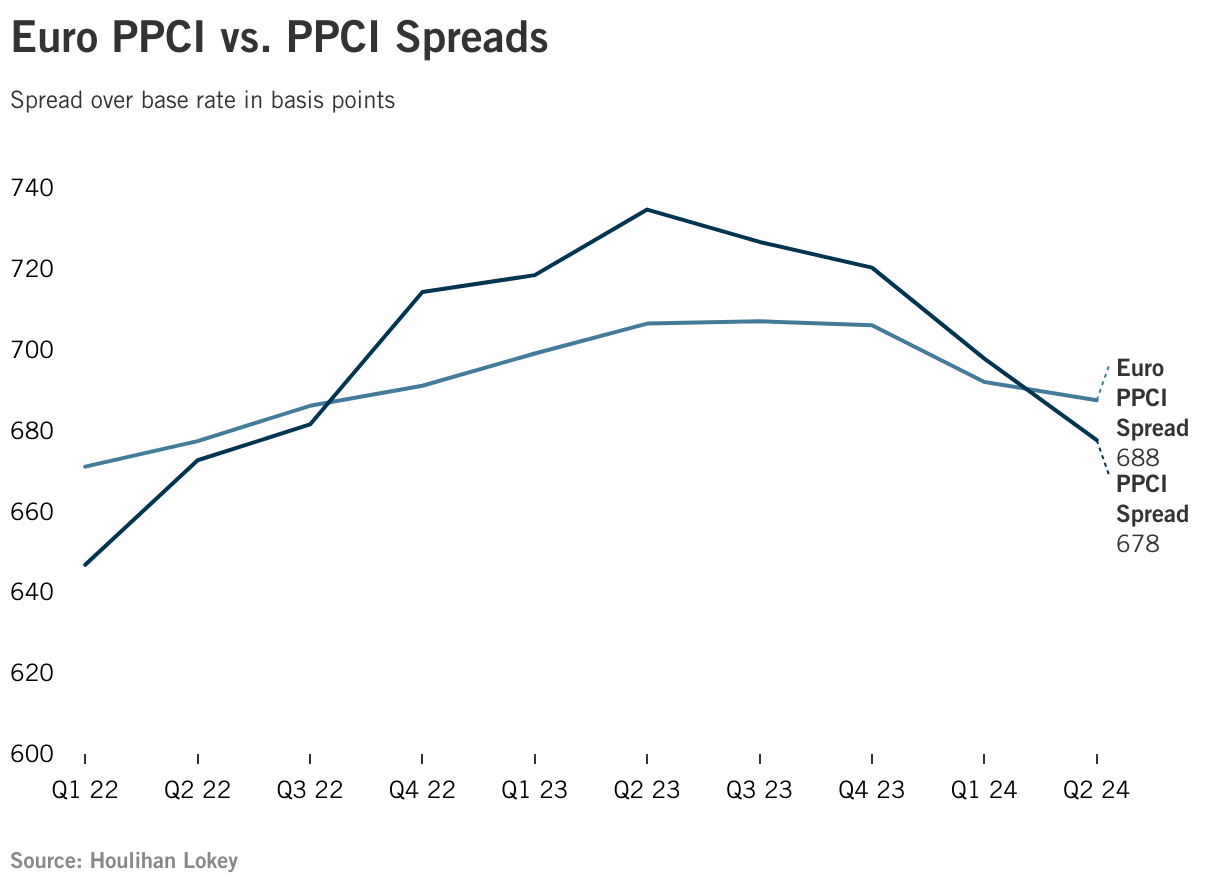

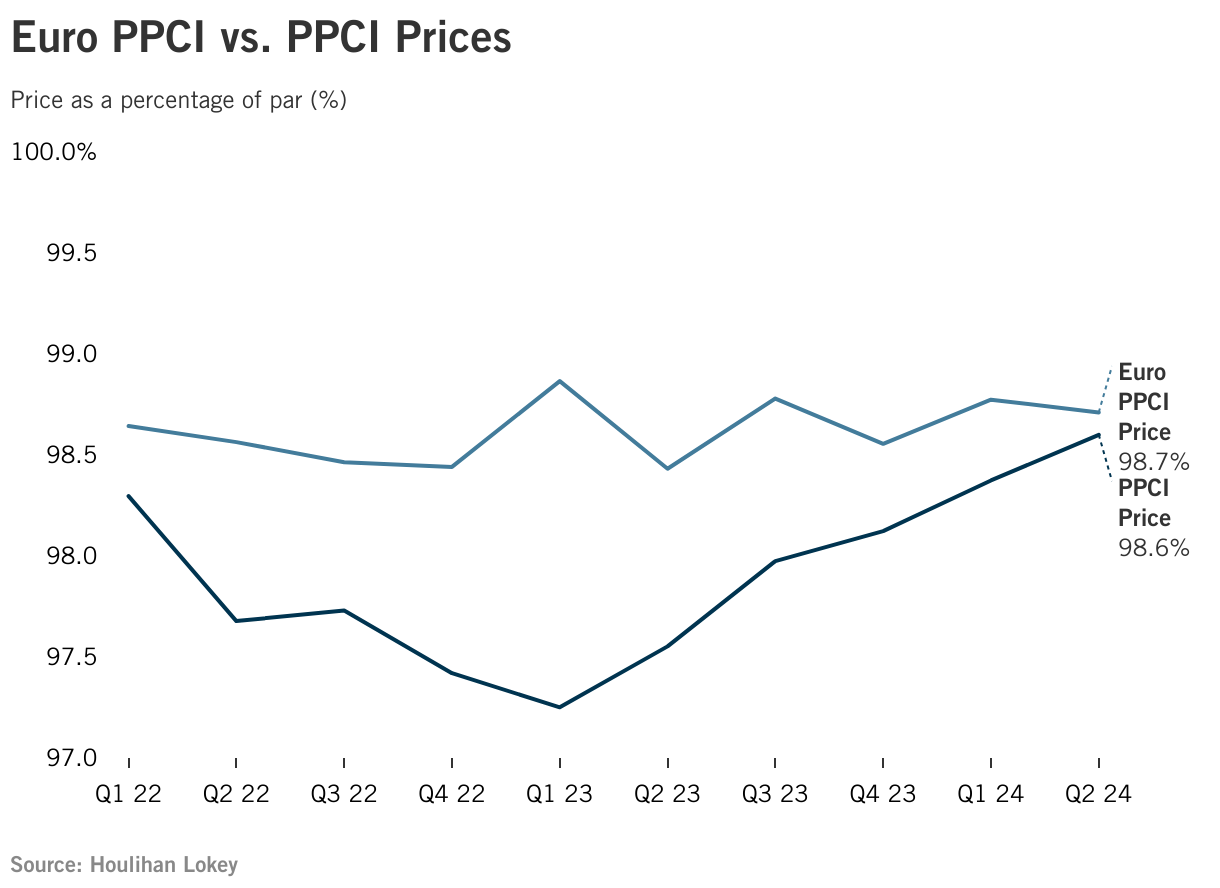

While the European private credit market is still significantly smaller in size and less mature than the North American private credit market, the charts below from the European PPCI illustrate that European private credit spreads and price trends have been broadly similar to those in the U.S. private credit market. Spreads are the difference between the prevailing at-market yield and the base rate.

Comparison Between North American and European Private Credit Markets

Yields in the European subset of the PPCI are currently 10 bps lower than the USD-majority PPCI. The overall difference can be attributed to the lower base rate environment in Europe, partially offset by recent interest rate cuts in the U.S.

Contacts

-

Dr. Cindy Ma Managing Director Global Head of Portfolio Valuation and Fund Advisory Services

-

Milko Pavlov Managing Director Financial and Valuation Advisory

-

Chris Cessna, CPA, CFA Managing Director

-

Vidur Taneja Director

-

Joseph Cristantiello Director