Private Performing Credit Index—Q1 2024

Introduction

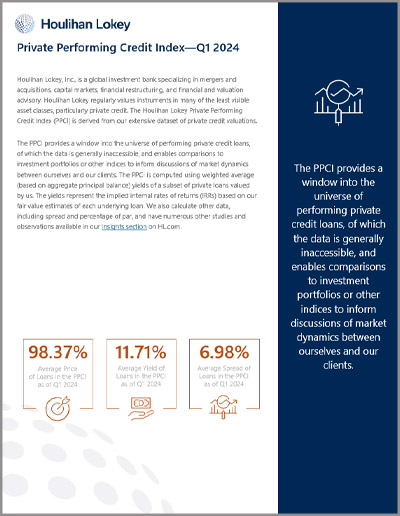

Houlihan Lokey, Inc. (NYSE:HLI) is a global investment bank with expertise in mergers and acquisitions, capital markets, financial restructuring, and financial and valuation advisory. Houlihan Lokey regularly values instruments in many of the least visible asset classes, particularly private credit. The Houlihan Lokey Private Performing Credit Index (PPCI) is derived from our extensive dataset of private credit valuations.

The PPCI provides a window into the universe of performing private credit loans, of which the data is generally inaccessible, and enables comparisons to investment portfolios or other indices to inform discussions of market dynamics between ourselves and our clients. The PPCI is computed using weighted average (based on aggregate principal balance) yields of a subset of private loans valued by us. The yields represent the implied internal rates of returns (IRRs) based on our fair value estimates of each underlying loan. We also calculate other data, including spread and percentage of par, and have numerous other studies and observations available in our Insights section on HL.com.

As of Q1 2024, the loans in the PPCI had a weighted average:

Price of 98.37%

Yield of 11.71%

Spread of 6.98%

Results

Many investment factors drive both borrowers and lenders to the private credit markets. Two of the publicly available indices are informative in these discussions of private vs. public credit and bonds vs. loans. The chart below illustrates those differences.

LL100 – Leveraged Loan 100 – An index of the largest 100 broadly syndicated loans as compiled and published by S&P Global

BAML – U.S. HY Master Trust II – a compilation of high-yield bonds by ICE/BAML

Change From Previous Quarter

From December 31, 2023, to March 31, 2024, the PPCI decreased by 1 bp, from 11.72% to 11.71%. With each PPCI release, our Private Credit team reviews the data (which consists of 11,793 qualifying quarterly asset valuations performed since September 30, 2017), market conditions, and changes in the composition of the portfolio to explain the difference from the previous quarter. Our analyses focus on the significant drivers of differences to aid our clients when comparing their own observations of the market yields; however, the change in composition may affect the index in a specific way that is not consistent with general experience. Additionally, the changes below reflect the absolute changes in each metric quarter over quarter and are not meant to be cumulative changes that bridge PPCI yield values from one quarter to the next.

-

- Benchmark Rates

The yield is the discount rate that makes the present value of future cash flows equal to the loan value. The SOFR swap rate for the relevant average maturity increased approximately 49 bps from December 31, 2023, to March 31, 2024. A significant portion of loans in the index were transitioned from LIBOR to SOFR during the quarter ending September 30, 2023. As a result, we have shifted our benchmark rate from LIBOR to SOFR for the purposes of this comparison. - Coupon

The coupon represents the contractual interest margin above the applicable base rate for floating rate loans and represents the contractual interest rate for fixed-rate loans. The weighted average coupon decreased by 1 bp from December 31, 2023. - Price

The weighted average price for loans in the PPCI increased from 98.12% on December 31, 2023, to 98.37% of par on March 31, 2024. - Spread

Spread is added to the base rate to form the discount rate. The weighted average spread for loans in the PPCI decreased from 720 bps on December 31, 2023, to 698 bps on March 31, 2024, representing a decrease of 22 bps. - Composition

Although a significant portion of the PPCI is composed of loans valued in prior periods, some change occurs. The change in index components contributed to a decrease of 18 bps in the PPCI IRR from December 31, 2023, to March 31, 2024.

- Benchmark Rates

*The file is an Adobe Acrobat PDF. If you experience difficulty opening the downloadable file, you may need to download the free Acrobat Reader.

Further Information or Analysis

To receive further information or discuss Houlihan Lokey’s PPCI, please contact our Portfolio Valuation team:

Houlihan Lokey’s Portfolio Valuation and Fund Advisory Services practice is a leading advisor to many of the world’s largest asset managers, who rely on its strong reputation with regulators, auditors, and investors; private company, structured products, and derivatives valuation experience; and independent voice.

Contacts

-

Dr. Cindy Ma Managing Director Global Head of Portfolio Valuation and Fund Advisory Services

-

Chris Cessna, CPA, CFA Director